Ireland

Select another country here:

[display-map id=’10797′]

Composition of the Irish seafood sector

In 2015, Irish fishing companies generated EUR 244 million in landings income (Table 42). Processing companies generated a further EUR 646 million in production revenue.

Ireland had a trade surplus of EUR 292 million in fish and fish products in 2016. It exported EUR 555 million. Three quarters of Irelands fish exports were to EU countries. The main export destinations of Irish fish and fish products were France (26%), Spain (14%) and the United Kingdom (11%).

90% of Ireland’s EUR 263 million fish imports were from EU countries. Its main import partners were the United Kingdom (65%), Germany (7%) and France (6%).

Ireland had 1,953 registered commercial fishing vessels in 2017, of these 69% were active. These vessels were owned by 1,885 enterprises. 175 enterprises – 9% of all fishing enterprises – owned more than one vessel.

The Irish fish catching segment employed 2,522 FTE. The Irish fish processing segment employed a slightly smaller workforce of 2,147 FTE.

Ireland is surrounded by some of the most productive fishing grounds in the EU. Hence, coastal communities in the country have always been economically and socially reliant on the fishing sector. According to estimates, the GDP of the Irish seafood sector was EUR 1.1 billion (0.36% of total GDP) in 2016 and the sector employed over 11,000 workers. From 2008 to 2016, the number of people employed in the fish catching sector increased from 2,866 to 3,358 (BIM, 2016; Carpenter & Kleinjans, 2017). In 2016, total value of landings in Ireland accounted for 6.5% of total EU landings by value and 6% by volume (264,000 tonnes) (Eurostat 2018). The two biggest fishing ports by value of landings are Castletownbere

(EUR 111 million in 2016) and Killybegs (EUR 85 million in 2016) (BIM, 2016; Carpenter & Kleinjans, 2017).

As of 2018, the Irish fleet comprises 1,987 vessels – 86% of which are under 12 m vessels. This represents a 2% increase in the total number of vessels in the fleet in comparison with 2008. Total capacity of the fleet in 2017 was 63,921 GT and engine capacity of 189,291kW (DAFM, 2018).

The Department of Agriculture, Food and the Marine (DAFM) divides the national fishing fleet into four main segments, excluding the aquaculture segment (DAFM, 2018):

- A Refrigerated Seawater (RSW) Pelagic segment, mainly engaged in fishing for pelagic species such as herring, mackerel and blue whiting. This segment comprises 23 vessels.

- A Beam Trawler segment with vessels predominantly fishing in Irish inshore waters except in the southeast, where it targets flatfish such as sole and plaice. Currently ten vessels are officially registered as beam trawlers.

- A Polyvalent segment, accounting for the vast majority of the fleet (1,708 vessels in 2018, or 83%). This segment comprises a variety of vessels of different sizes and different gear types, including small inshore vessels (netters and potters), and medium and large offshore vessels targeting whitefish, pelagics and molluscs.

- A Specific segment including vessels which are permitted to fish for bivalve molluscs and aquaculture species. This segment comprises 147 vessels.

In 2016, Ireland counted 156 seafood processing companies employing 2,147 FTE (see Table 42). Of these, 16% had revenues over EUR 10 million, 33% between EUR 1 and EUR 10 million, and the remainder (51%) less than EUR 1 million. Most of the Irish seafood processing companies comprise less than ten employees (EC Representation in Ireland, 2018). Whitefish and multi-species processing sites account for 44% of total sites, shellfish for 25%, salmonids for 21% and pelagic for 10%.

Besides the processing facilities associated with the fishing companies described below, the following companies are specialised in seafood processing. A complete list of all Irish registered fish buyers was published by the Sea-Fisheries Protection Authority (SFPA) and can be found online (Sea-Fisheries Protection Authority, 2018).

- Green Isle and Donegal Catch

Green Isle Seafood is the largest processor of white fish in Ireland with 3,000 metric tonnes annual production capacity. Green Isle Seafood owns Donegal Catch, one of Ireland’s major frozen fish brand. The company processes a wide range of species that are sold to the wholesale, foodservice and retail sectors throughout Europe (Green Isle Foods, 2018).

- Ocean Path

Ocean Path is one of Ireland’s biggest seafood processors. The company supplies fresh and smoked fish to all major Irish retailers as well as exporting to places such as Dubai and Singapore (Ocean Path, 2018). In March 2018, Ocean Path was bought by Iceland Seafood International, a major company in exports of seafood from Iceland to all main markets around the world (Irish Independent, 2018).

- Irish Fish Canners

Irish Fish Canners is the only fish canning facility in Ireland, based in North West County Donegal. It specialises in the canning of pelagic species (herring, mackerel and sardine) and supplies markets both domestically and internationally. The company is a co-packing business for Irish market leader John West. In 2015, Irish Fish Canners launched its own canned mackerel brand: the Irish Atlantic Canned Fish brand (Irish Canner, 2018).

- Krijn Verwijs (Netherlands)

Krijn Verwijs Yerseke B.V. is one of the largest players in the European crustaceans and shellfish market. The company specialises in the marketing of mussels, oysters, lobsters and various types of shellfish, which partially originate from Ireland. Mussels are supplied to supermarket chains and wholesalers in Europe under the brand name Premier and other private labels (Krijn Verwijs Yerseke, 2018).

About half the fish and fish products that enter the Irish food market is sold as fresh. 32% is sold as frozen. Dried/smoked/salted fish accounts for 13% of all fish and fish products sold in Ireland. Similar to other countries, three quarters of all fish and fish products are sold through retail outlets, the remainder is sold in the food service industry. Slightly less than 75% of both fresh and frozen fish products are sold through retail outlets, whereas approximately 85% of both canned and dried/smoked/salted fish and fish products are sold through retail (see Figure 58).

Different from countries such as France (see Chapter 10) and Greece (see Chapter 0), the vast majority (90%) of fresh fish sold through Irish retailers is sold as branded. The remainder is sold under retailers’ own label. The proportion for canned and frozen are slightly lower. Respectively 69% and 67% of those categories is sold as branded, with the remainder sold under own labels.

A key brand for fresh fish in Ireland is Keohane’s Seafood with a market share of approximately 30% of the fresh segment. Iglo (part of Nomad (UK)) is the market leader in the Irish frozen fish segment with a market share of around 31%, while the frozen brands of 2 Sisters Food Group have a market share of around 28%. In the canned segment, the John West brand of Thai Union (Thailand) holds around 56% of the market, while Princes (part of Mitsubishi (Japan)) accounts for approximately 14%. Dunn’s of Dublin (part of Oceanpath) holds a share of around 49% of the dried/smoked/salted fish segment in Ireland, while HJ Nolan, Irish Seaspray, Quinlan’s Kerry Fish and Carr & Sons hold a share of approximately 10% each in this segment (FFT, 2018).

Producer organisations

Ireland has five EU recognised POs (Table 44) under the umbrella of the Federation of Irish Fishermen (FIF), formed in 2007. Due to lack of data availability, the number of vessels and members is not provided.

In Ireland, quota is a public resource managed to ensure that property rights are not granted to individual vessel owners. The Quota Management Advisory Committee (QMAC) meets monthly to advise the DAFM Minister in their decision-making process regarding quota allocation for particular fish stocks, mainly whitefish. Pelagic fisheries are generally managed on a seasonal basis (spring and autumn months). The QMAC is composed of fishing industry representatives: one member from each of the four national Fisheries Producer Organisations (PO), one member from the National Inshore Fisheries Forum, one member from the Fish Producers and Exporters Association and one member of the Fishing Co-Operative Association. The Minister follows their recommendations as far as possible (DAFM, 2018; Carpenter & Kleinjans, 2017).

Irish Fish Producers’ Organisation (IFPO)

The IFPO was the first PO established in Ireland, in 1975. It is comprised of fishers based throughout the Irish coastline. The IFPO represents fishers engaged in pelagic, whitefish, shellfish and inshore sectors. The Board of Directors of the Organisation is elected by members and is currently constituted of nine representatives (Irish Fish Producers’ Organisation, 2018).

Killybegs Fishermen’s Organisation Ltd. (KFO)

The KFO was recognised as a PO in 1985 and is the largest PO in Ireland, with members throughout the country. It represents fishers in pelagic, whitefish and shellfish sectors. Of the 23 RSW pelagic vessels in Ireland, 20 are members of KFO (Fish Info & Services, 2018).

Irish Seafood Producers’ Group Ltd (ISPG)

The ISPG was established by a small group of independent Irish fish farmers in 1985. It is now the principal organisation for the sales and marketing of Irish farmed finfish products and is Ireland’s leading supplier of organic salmon and trout farmed at sea. The ISPG’s marine sites are located along the Irish Atlantic Coast (Irish Seafood Producers Group, 2018).

Irish South & West Fish Producers Organisation Ltd. (IS&WFPO)

The IS&WFPO was created in 1994. The Organisation represents coastal fishers in the south and west coast of Ireland. Its members are mostly owners of whitefish vessels ranging from 12 to 30 m. The organisational structure consists of a Chairman, Secretary, Manager and a Board of Directors, currently comprising 11 Directors (The Irish South and West Fish Producers Organisation, 2018).

Irish South and East Fish Producers (IS&EFPO)

The IS&ESPO was recognised as an official PO in 2013 and is based in Waterford. Its members are part of the coastal fishing fleet (European Commission, 2018). No additional information could be found on the IS&EFPO.

Company analysis

This section provides an analysis of the company structures of six of the most important fish catching companies active in Ireland. The section is organized as follows: section 13.3.1 presents analyses of the company structures of fishing enterprises engaged predominantly in the pelagic segment; and section 13.3.2 focuses on a company active in the demersal segment.

Pelagic segment

Atlantic Dawn Group

The Atlantic Dawn Group was established in 1968. The company is a world leader in the catching and processing of pelagic fish, which are generally sold frozen. The Atlantic Dawn Group operates its own fleet, in addition to a number of independently owned vessels. Its 13 vessels are equipped with either purse seines or trawlers. The Group also owns and operates two shore freezing facilities: Arctic Fish Processing located at the company’s homeport in Killybegs; and Atlantic Dawn Seafoods A/S located on the Island of Smola in Norway. Products are sold unbranded, in bulk, and 99% of the production is exported worldwide, mostly to buyers located in West Africa, Russia and the Far East (Atlantic Dawn, 2018). Together with the Norwegian Ostervold and Hufthamer families, Atlantic Dawn also operates vessel leasing and aquaculture enterprises.

The company’s current directors are Niall O’Gorman and Karl McHugh (Company Registration Office, 2018a).

The description above has shown that Atlantic Dawn is both vertically and horizontally integrated. It has activities all down the seafood value chain from fish catching and processing to distribution. Moreover, it has a sizeable fleet in Ireland, as well as aquaculture activities in both Ireland and Norway, indicating horizontal integration. Director Niall O’Gorman is on the board of Irish Pelagic – a Dutch Jaczon subsidiary (see section 18.3.2) – indicating also potential informal integration (Svensson, 2013).

Gallagher Bros (Fish Merchants)

Gallagher Bros (Fish Merchants) is a family run business based in Killybegs, established in 1919. The company specialises in the catching and primary processing of pelagic species such as mackerel, herring and blue whiting. The company has three processing plants in County Donegal. Final products range from whole frozen to marinated skinless fillets. All sales are in bulk to secondary processors in Europe, USA, Japan, Korea, China, West Africa and Egypt (100% exported). Gallagher Bros own Ocean Trawlers Ltd., which operates RSW pelagic vessels out of the port of Killybegs, and Ocean Farm Ltd., a salmon farming company located in Donegal Bay (Gallagher Bros, 2018).

The company’s current directors are Tadhg Gallagher, Anne Gallagher, Michael Gallagher and Patrick Gallagher. As at 31st July 2017, Gallagher Bros’ Ocean Trawlers Ltd. had net assets of EUR 7 million and employed a total of 12 people (Company Registration Office, 2018b.)

The description and company structure shows signs of both vertical and horizontal integration. The company operates processing plants, indicating structural vertical integration. The company also operates more than one vessel, a sign of horizontal integration through fleet expansion.

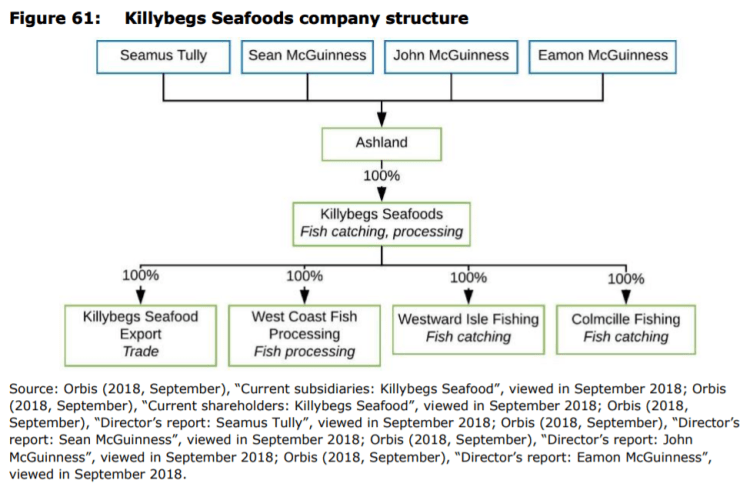

Killybegs Seafoods

Killybegs Seafoods was established in 1986. Its principal activity is the primary processing of pelagic species. Raw material is sourced from the North West Atlantic waters and brought to the factory by RSW trawlers. The company contracts six Irish fishing vessels, of which it owns 3. To a lesser extent Killybegs Seafoods also receives supplies of raw material from other Irish, UK and Norwegian vessels. Products are sold under the Killybegs Seafoods brand. Export markets (99% of total production) are primarily the Far East, Russia, Europe, Egypt and West Africa (Killybegs Seafood, 2018).

The company’s current directors are Sean McGuinness and Seamus Tully. As at 31st March 2017, Killybegs Seafoods (Export) Ltd. had net assets of EUR 140,786 (Company Registration Office, 2018c).

The analysis above has shown that Killybegs Seafoods is part of a both vertically and horizontally integrated group. Horizontal integration is evident through its fleet size and the number of the fish catching subsidiaries. Vertical integration is seen in Killybegs Seafoods’ business activities in three stages of the seafood value chain: fish catching, processing and trade.

Demersal segment

Saltees Fish

Saltees Fish is a family owned business founded in 1996, based in Kilmore Quay (County Wexford, South East of Ireland). The company specialises in fresh whole and filleted whitefish (mostly megrims and monkfish) and prawns. It is engaged in catching, handling and processing of fish caught from its own fleet of trawlers for supply to the domestic and export market. Forty percent of Saltees Fish products are sold domestically, while 60% reach European markets, mainly Spain, France, Belgium, Holland and Italy. The owners of the company, the O’Flaherty Brothers, operate over ten beam trawlers, three twin riggers and a pelagic vessel. Michael O’Flaherty is the current Managing Director of Saltees Fish (Saltees Fish, 2018).

The analysis above has shown that Saltees Fish is both vertically and horizontally integrated. Horizontal integration is evident through the size of its fleet and the number of fish catching subsidiaries. Moreover, horizontal integration is cross-segment, i.e. Saltees is active in both the demersal and pelagic segments. As the company is active in fish catching and wholesale, it is also a vertically integrated company. Denis O’Flaherty stated that the company does not have processing operations as the market prefers non-processed whitefish (O’Flaherty, 2018).

Integration

The analysis shows that there is both vertical and horizontal integration taking place in the Irish seafood value chain. Most fishing companies and vessels in Ireland are owned by fishermen (i.e. not big companies owning several vessels). Hence, there is not much integration, only a few companies own both vessels and a factory/factories (Murphy, 2018).

Donal Buckley, Director of Business Development and Innovation Services at BIM (Ireland’s Seafood Development Agency), states that the levels and forms of vertical integration depend on the sector. He states that the pelagic sector is generally integrated, as companies are a mix of vessels and processing factories. This segment accounts for one third of the seafood sector in Ireland. The shellfish sector also has processing companies. These buy raw material directly from the fishing vessels. For whitefish and crustaceans, cooperatives are the first point of landing. These cooperatives then sell to processing companies on a supply basis (Buckley, 2018). Some of these cooperatives have become businesses (O’Flaherty, 2018).

Pelagic companies are investing in processing to develop value added products and the processing of by-products (Buckley, 2018). Pelagic companies harvest large amounts of fish, and have access to sufficient quota (O’Donoghue, 2018). Therefore, they can open factories as they have sufficient supply. Factories need access to quota/large amounts of raw materials; hence smaller processing companies cannot compete. Smaller processing companies generally do not own boats (Murphy, 2018). It is generally the vessel owners which invest in processing facilities, rather than the other way around. Processing companies also invest in vessels but not as much as fish quota in Ireland is a public resource (Buckley, 2018; O’Donoghue, 2018). However, some processing companies develop supplier alliances (Buckley, 2018).

Ireland is very bureaucratic and expensive to invest in processing (O’Flaherty, 2018). Currently, there is a lack of scale to be able to compete on the market for the processing industry. Moreover, there is a lot of legislation involved in fishing (for nets, gear, training, monitoring, quotas, hygiene, safety etc.). Traditional fishermen can’t cope with it, it is financially and timewise impossible. On the contrary, big companies get into a pattern, they have staff that only deals with this, so it is easy/ manageable for them (O’Donoghue, 2018). Due to this and other factors, Murphy claims that small companies are being wiped out as big companies are taking over (Murphy, 2018).

There is relatively limited foreign ownership in the Irish seafood sector. Companies are mainly Irish-owned (approximately 80%), although there is an increase in international investments in aquaculture and processing (Buckley, 2018).

One of the effects of integration has been an increase in employment in the processing sector. As the fish harvest does not increase so much, there is no increase of labour on the vessels, however, there is increasingly more in the processing sector (Buckley, 2018). Nevertheless, as processing facilities modernise, the employment opportunities decrease (Murphy, 2018). This happened in Ireland especially over the last decade (Murphy, 2018).

There are over 160 fishing companies in Ireland, 40 of which continue investing in their company, 20 to 25 significantly, mainly in processing where value is added to the products, but also in vessels for efficiency – mainly in gear technology to manage the landing obligation (Buckley, 2018). The landing obligation has meant that companies are making investments at boat level to increase efficiency (Buckley, 2018).

There are concerns about Brexit. It is expected that UK boats will head towards Irish waters. Patrick Murphy from the Irish South & West Fish Producers Organisation argues that the relative stability measure will have to change. If not, small fishing companies will not survive (Murphy, 2018).

There are no quota swaps and there is no quota leasing or similar practices, as quota is not privately owned. Fishing quota in Ireland belongs to the state, i.e. is not privately allocated to licenses linked to vessels. Hence, it does not make sense to buy several vessels as a company to own more quota. Quota is allocated monthly which forces boats to implement expensive modernisation to be efficient. Ever fewer boats are going to sea. Only fishermen (or companies) that can afford modernisation are able to compete. This has led to important changes in the dynamic of coastal communities over the last couple of decades (Murphy, 2018).

0 Comments