Italy

Select another country here:

[display-map id=’10798′]

Composition of the Italian seafood sector

In 2015, Italian fish catching companies generated EUR 894 million in landings income (Table 45). Fish processing companies generated EUR 2.5 billion in production revenue.

Italy had a fish and fish product trade deficit of EUR 4.9 billion in 2016. It exported fish worth EUR 675, while it imported EUR 5.5 billion. It imported 60% of its fish from EU countries. Italy’s main import partners were Spain (21%), the Netherlands (6%) and Denmark (6%).

81% of Italy’s fish and fish product exports were destined to other EU countries. The main export destinations for Italian fish products were Spain (19%), Germany (12%) and France (9%).

In 2015, there were 12,426 registered commercial fishing vessels in Italy. These were owned by 8,004 enterprises. 1,166 enterprises (15% of all fishing enterprises) owned more than one vessel.

The Italian fish catching segment employed 21,459 FTE. The average employment per vessel was therefore 1.7 FTE. This indicates the full-time nature of the Italian fishing segment. The fish processing segment employed a far smaller workforce at 2,388 FTE.

Italy’s coastline is around 9,000 km long. The length of the coastal regions is about 10 % of the EU total.

Between 2010 and 2017, the total number of vessels decreased from 17,367 to 12,310 (Eurofish, 2018; STECF 2018). Meanwhile, marine catches dropped by 44% between 2006 and 2014. Italy’s fleet is highly diversified with a broad range of vessel types targeting different species, predominantly in the Mediterranean Sea. Small-scale fishing vessels account for the largest segment within the fleet (8,763 vessels), followed by trawlers (2,542 vessels), and hydraulic dredges (706) (Eurofish, 2018).

Due to international and European management measures, the number of Italian vessels involved in Bluefin tuna fishing decreased from 98 in 2000, to 48 in 2009, to 12 in 2011. In 2018, the EU decided to increase the TAC for Italy. The extra quota was distributed inter alia among three other vessels. Therefore, currently 15 vessels are authorized for Bluefin tuna fishery. A Ministerial Decree of 28 May 2010 prescribes 130 tonnes as the minimum capacity of vessels practicing the seine fishing method, which is used for fishing Bluefin tuna (Ferrigno, 2018).

The main species targeted in Italy are small pelagics like anchovy and sardine. The main large pelagics that are landed are Bluefin tuna, albacore and swordfish. Among demersal fish, most caught are hake and red mullet. An important portion of total Italian landings is cephalopods, comprising cuttlefish, octopus, and horned octopus. The deep-water rose shrimp and the spot tail mantis shrimp are the most important crustaceans landed. “The catch composition of marine fisheries is very heterogeneous, reflecting both the different gears in use, various fishing grounds, and the high biodiversity of aquatic resources” (Eurofish, 2018).”

Just over 70% of the fish and fish products that enter the Italian seafood market are sold as fresh. 10% is sold canned, 12% as frozen, and the remainder as dried/smoked/salted. Similar to other countries, approximately three quarters of the fish and fish products sold in Italy are sold through retail outlets, the remaining 25% is sold in the food service industry. 71% of fresh fish is sold through retail outlets, the remainder through food service establishments (see Figure 63). More than 80% each of the other fish and fish product categories are sold through retailers.

The vast majority of fresh fish (87%) is sold unbranded in retail outlets, only 13% is sold as branded. None of the other categories is sold unbranded (see Table 46). More than 80% of canned and frozen fish products sold in Italy are sold as branded, the remainder is marketed with the retailers’ own labels.

As brands only play a minor role in fresh seafood in Italy, none of them hold a large market share. Finpesca accounts for approximately 2% of the fresh fish market in Italy, Azzurra Pesca holds a share of 1%. In the frozen fish products segment, Iglo (Nomad (UK)) accounts for about 35% of the market, Pescanova Italia (part of Pescanova (Spain) (see section 23.3.3)) has a share of around 10% in the frozen segment in Italy. In the canned fish products segment, Bolton Group (Netherlands) with brands such as Saupiquet and Rio Mare holds a share of approximately 31%, Grupo Calvo (Spain) with its Nostromo brand holds a share of approximately 11%. In the dried/smoked/salted product segment, Fjord (acquired by Agroittica Lombarda in late 2017) holds a share of around 15% of the Italian market, Coam’s brands account for a share of around 6% (FFT, 2018).

Producer organisations

Table 47 provides an overview of the 43 producer organisations in Italy, currently recognized by the European Union authorities. Due to lack of data availability, the number of vessels and members is not provided.

Table 48 provides an overview of the producer organisation associations. There are two producer organisation associations in Italy: The Feder.OP and the Associazione nazionale di organizzazzioni di produttori del settore ittico. Mario Bello, president of the Feder.OP, states that POs receive too little funding to bring about ambitious plans of market restructuring. Restructuring is necessary as the Italian fisheries sector is going through a deep crisis (Bello, 2018).

Not much information about the other producer organisation association could be found as there is no website. They are recognized by the Italian government (Gazzetta Ufficiale, 2010).

Company analysis

According to a company screening, the list of top-6 fishing companies in Italy, based on revenues, is led by Asaro Matteo Cosimo Vincenzo S.R.L., with revenues of EUR 14.7 million in 2016 and 45 employees. The next biggest fishing company, Azzurra Pesca S.R.L. Unipersonale, had revenues of EUR 4.1 million and only seven employees (see Table 49).

Asaro Matteo Cosimo Vincenzo

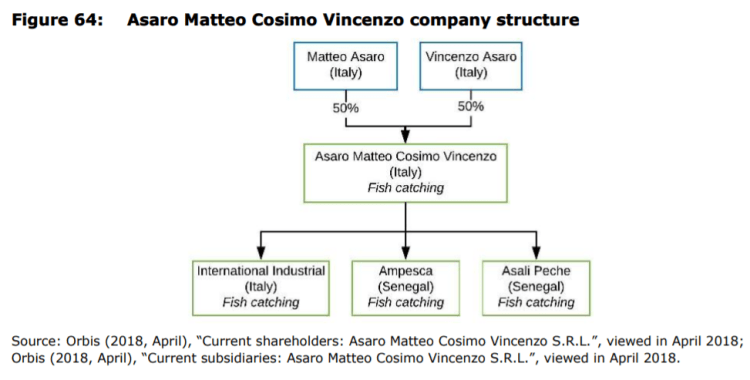

As Table 49 shows, Asaro Matteo Cosimo Vincenzo had the largest revenues and most employees in 2016. Figure 64 provides an overview of the Asaro Matteo Cosimo Vincenzo company structure. Matteo Asaro and Vincenzo Asaro are the ultimate owners of Asaro Matteo Cosimo Vincenzo. Both of them hold 50% of the company. Asaro Matteo Cosimo Vincenzo owns 13 vessels. The subsidiary International Industrial owns one vessel. Three of the vessels owned by Asaro Matteo Cosimo Vincenzo operate in Senegal, the others are operating in Italy.

Asaro Matteo Cosimo Vincenzo used to fish only near the Italian coast, but around 1960, thanks to new technologies that allowed the onboard freezing, they extended their fishing area to the Eastern Central part of the Atlantic Ocean (FAO area 34) and the Mediterranean Sea and the Black Sea (FAO area 37).

Two other companies are registered at the same address as Asara Matteo Cosimo Vincenzo: Asaro Pesca and Asaro Seafood. Asaro Pesca – a restaurant – has two shareholders, namely Salvatore Asaro owning 99% of the shares, and Caterina Vannutelli owning the remaining 1%. Asaro Seafood is owned by Pasquale Asaro. Both companies seem to be engaged in processing and marketing fish (Asaro Seafood, n.d. and Pagine Gialle, n.d.). It is likely that these individuals are relatives of the owners of Asara Matteo Cosimo Vincenzo.

The analysis above shows that the company is integrated horizontally. This is evident through the size of its fleet, and its investments in vessels active in Senegal. Asara Matteo Cosimo Vincenzo may be vertically integrated through relations with the fish processing and marketing companies registered at the same address and owned by individuals which share their family names with the owners of Asara Matteo Cosimo Vincenzo.

Azzurra Pesca S.R.L. Unipersonale

Azzurra Pesca is a medium-sized fishing company, founded in 1983 by the Catania brothers. In 2015, the company expanded with Pesce Azzurro Med, a company aimed at marketing preserved fish products, with its headquarters in Morocco (Azzurra Pesca. n.d.).

The company owns two vessels. Its trawler is a 46m tuna trap called Angelo Catania, which has the third highest ICCAT quota (Maximum fishing capacity of Bluefin tuna) in Italy. Its main activity is fishing Bluefin tuna, from 25 May to 25 June, while in the remaining months of the year it focuses on anchovies and sardines. The smaller vessel – Padre Pio – is a support boat to the trawler during the Bluefin tuna fishing. Like Angelo Catania, during most of the year it is used for fishing anchovies and sardines. The company operates in the Mediterranean, coastal and lagoon fishing sector in inland waters (Azzurra Pesca, n.d.a).

Azzurra Pesca markets a brand of fish products (Azzurra Pesca, n.d.b).

Together with Testa Giuseppe (see section 14.3.3), Pescatori San Pietro Apostolo (see section 14.3.4) and Pescatori La Tonnara Societa’ Cooperativa (see section 14.3.6), Azzurra Pesca is one of the owners of the Consorzio Marenostrum Tuna. This consortium was created in 2012 for the promotion of Bluefin tuna in Italy and is based in Salerno. At the time the new organization started, nine of the (then) twelve national vessels authorized to tuna fisheries joined, with the aim of involving all the Italian quota assigned to this trade (Ansa, 2012).

The above analysis illustrates that Azzurra Pesca is both vertically and horizontally integrated. Levels of horizontal integration are small as the company only operates two vessels. However, these vessels target different species during the course of the year indicating portfolio diversification. Azzurra Pesca is vertically integrated as it not only harvests fish, it also processes and markets them under the brand Azzurra and is engaged in gastronomy in Morocco.

Testa Giuseppe

Testa Giuseppe is based in Ognina, Catania. The company currently has four shareholders, all Testa family members. The Testa family has been active in the fishery sector for over 200 years (Testa, 2018).

The core business of the company is Bluefin tuna fishing, but involvement in the segment of small pelagic species has allowed the company to stabilize production and ensure occupational stability (Testa, 2018). The company owns a 45m vessel, called Atlante, which was authorised for Bluefin tuna fishing after the company in 2010 collected quota from other vessels. Testa Giuseppe acquired a second vessel in 2012, the Futura Prima, which was also intended for tuna fishing, but it did not meet the requirements (130 tonnes criterium). It supports the bigger vessel during the Bluefin tuna fishing season, and during the rest of the year it is active in fishing small pelagic species. The small pelagic fishing activities are mainly around the Aeolian Islands and the Ionian Sea, whereas the Bluefin tuna fishing takes place in the Tyrrhenian area around Calabria (Testa, 2018).

Both investments, buying the quota and buying the second vessel, had various drivers: remaining in the market of Bluefin tuna fishing and stabilizing the company revenues (Testa, 2018).

The bigger vessel is involved in research and promotional activities outside the fishing season for Bluefin tuna (Testa, 2018).

Whereas its main activity is fishing, the company has recently established a processing plant in Porto Palo di Capo Passero (Southern Sicily). The processing plant enables the company to process the fish on a daily basis and closer to the source, which increases the quality and the value of the product. Although the plant has been active only for about one year, the objective for the future is to further pursue the integration process into the marketing and retailing segments (Testa, 2018). Testa has its own brand ‘Testa Conserve’.

Together with Azzurra Pesca (see section 14.3.2), Pescatori San Pietro Apostolo (see section 14.3.4) and Pescatori La Tonnara Societa’ Cooperativa (see section 14.3.6) the company is one of the owners of the Consorzio Marenostrum Tuna.

Figure 66 shows the company structure of Testa Guiseppe.

Similar to Azzurra Pesca (see section 14.3.2), Testa Giuseppe has engaged in limited horizontal integration. However, it has concentrated its quotas onto one vessel. With the establishment of its processing plant and marketing its own brand of fish products – Testa Conserve – it has engaged in vertical integration.

Pescatori San Pietro Apostolo

Pescatori San Pietro Apostolo has 35 shareholders, and a subsidiary, the Consorzio Marenostrum Tuna, which it jointly owns with Testa Giuseppe, Azzurra Pesca and Pescatori La Tonnara Societa’ Cooperativa. The company owns two vessels, San Pietro Uno and Sparviero Uno. Table 50 gives an overview of all the shareholders and the percentage of their ownership.

The ownership of two vessels points to limited horizontal integration. No signs of structural or informal vertical integration have been identified for the company.

Euro Pesca Cetara

Euro Pesca Cetara is a medium-sized company owned by seven shareholders. These seven shareholders are also shareholders of Pescatori San Pietro Apostolo. The company owns one ship, called Angela Madre.

The company structure does not show signs of structural or informal horizontal or vertical integration.

Pescatori La Tonnara Societa’ Cooperativa

The Pescatori La Tonnara Societa’ Cooperativa is a cooperative of fishers based in Cetara. Giovanni Aniello Ferrigno, president of the cooperative, says that around 70% of the Italian fishing fleet for Bluefin tuna is concentrated between Cetara and Salerno (Campania, Thyrrhenian coast). The history of the company reflects the developments in the Bluefin tuna fishing sector. In 2000, La Tonnara had three active vessels involved in Bluefin tuna fishing, in 2009, all the quota was allocated to one vessel, the Vergine del Rosario (to meet the 130 tonnes criterium). In 2018, a second vessel received quota for Bluefin tuna fishing. This is another of the three original vessels. The third vessel was scrapped.

Pescatori La Tonnara Societa’ Cooperativa is, like Testa Giuseppe, Azzurra Pesca and Pescatori San Pietro Apostolo, owner of the Consorzio Marenostrum Tuna.

The establishment of the 130 tonnes criterium (minimum capacity of a vessel) was the main driver of integration. La Tonnara has joined its quotas with that of the other members of the Consorzio degli Operatori del Tonno. The catch of each vessel is divided between the members of the Consorzio according to their respective shares (Ferrigno, 2018).

Integration

Levels of horizontal and vertical integration in Italy vary based on geography and targeted species (Basciano, 2018; Giachetta, 2018). The highest degree of integration has taken place in two segments: the tuna segment and the red and violet prawn segment. There is also some integration for pelagic fishing in the Northern and Mid regions of the Adriatic (Basciano, 2018). Offtake guarantees, access to large foreign markets (e.g. the Japanese market for Tuna), and quota increases have also been drivers for integration in the Italian seafood industry (Basciano, 2018; Giachetta, 2018).

Since the quota system was introduced for Bluefin tuna in the 2000s, this sector has seen a major organizational shift. Since the Ministry of Agricultural, Food and Forestry Policies has consistently distributed the biggest share of the Italian quota to seine fishing, companies have invested in this technique, which is quite costly. This has led towards the decrease of small-sized enterprises in favour of medium-sized ones (Basciano, 2018). This decrease was further driven by the decrease in overall TAC levels, which had led to a decrease in the fishing fleet (Giachetta, 2018). Horizontal integration in the tuna segment increased particularly between 2009 and 2011, with the adoption of conservation measures at both the European and the domestic level, and the reduced fleet size (Ferrigno, 2018; Bello, 2018). The establishment of the 130 tonnes minimum capacity criteria for seine fishing vessels was an important driver of consolidation (Ministerial Decree of 28 May, 2010). Operators with quotas on multiple vessels concentrated their quotas on a single vessel. Other operators tried to reach the 130 tonnes threshold by collaborating and joining their respective quotas together, e.g. within the Consorzio (Ferrigno, 2018). It is noteworthy that Italian companies have not tried to get access to larger quotas for Bluefin tuna by investing in other Mediterranean countries (Bello, 2018).

According to members of the Consorzio the joining of quotas is considered to be quite effective and successful. It offers a further incentive towards the establishment particularly of non-structural forms of horizontal organization. There is competition between the different groups. However, there is also strong sense of solidarity among the various operators involved in the seine fishing segment. Ferrigno – President of Pescatori La Tonnara – states that this sense of solidarity was the result of the TAC decreases for Italy in the 2009 to 2011 period (Ferrigno, 2018).

Other forms of horizontal integration in Italy are more limited. There is little integration in terms of quota transfers. In Italy it is only possible to buy or sell quotas distributed among producers using a specific technique (e.g. between purse seine fishing segment or longline fishing segment). Fishermen could theoretically sell or lease quotas to one another within the same PO, given that they are all involved in fishing with the same gear, e.g. seine fishing, but this does not happen in practice. Moreover, there is also no quota buying or selling at the international level (Giachetta, 2018).

Horizontal integration, as it has largely been driven by reduction in TACs and the consequent reduction in fleet size, has significant socio-economic impact. Livelihoods level are extremely low, and the sector is in sharp decline (Amoroso, 2018). Many producers had not yet recovered the costs of their recent investments in the sector when the catch restriction measures were introduced in 2009 to 2011 (Testa, 2018). Many people lost their jobs. In 2009, the scrapping policy did not spare very new vessels, which could not reach the 130 tonnes threshold. This was a loss in value for the sector (Ferrigno, 2018).

The contraction in the quota has allowed stocks to replenish. Between 2009 and 2018 there has been a strong increase in the number of brood stock fishes, as well as juveniles. The reduction of catch has also led to a price increase. While in 2005/06 the price was around EUR 3 to EUR 3.50 per kilo, today it has reached an average of EUR 10 per kilo (Ferrigno, 2018).

Vertical integration in the Bluefin tuna sector features an important regional dimension. Industrial fishery (seine fishing) is particularly widespread in Campania (South Tyrrhenian coast), whereas semi-industrial fishery (longline) is predominant in Sicily (Basciano, 2018). Nevertheless, there is very little vertical integration at the domestic level. Indeed, contrary to what happened for horizontal integration, the 2009 to 2011 contraction has weakened early forms of vertical integration that existed at the national level prior to 2010. Currently the quotas are only enough to meet the demands of the Japanese market. As such, there are few incentives towards devoting part of the catch to processing activities and to further vertical integration in Italy (Ferrigno, 2018).

Offtake arrangements – a form of non-structural vertical integration – play an important role in the Italian seafood value chain given the low level of development of the fish processing segment (Misuraca, 2018). Offtake agreements between fishing companies and traders tend to ensure a certain degree of stability for the few operators who are still active on the market (Misuraca, 2018). Offtake agreements for the small pelagic species segment and the Bluefin tuna segment are different (Giachetta, 2018). The former provide access to retailers in their final markets – Spanish and French retailers – while the latter provide access to intermediaries – Maltese and Spanish buyers – who then sell to the Japanese market (Bello, 2018; Ferrigno, 2018; Giachetta, 2018).

Offtake agreements are often considered the only solution for certain companies to remain in the business. Costs can only be covered through the anticipated payments of traders. Most of the landings of deep-water rose shrimp are exported to Spain. The strong reliance on this market, coupled with the fragmentation of Italian producers, has increased the leverage that Spanish buyers have on prices (Misuraca, 2018).

There is a strong regional difference in offtake arrangements. Fishing with trawl-pelagic nets is allowed in the Adriatic Sea, but it is forbidden in the Tyrrhenian Sea. As a result, while producers in the Adriatic Sea are able to ensure a stable supply, this is not the case for producers in the Tyrrhenian Sea. This, in turn, explains why there are offtake agreements in the Adriatic Sea. Regulatory differences in the different regions in Italy thus help or hamper vertical integration (Giachetta, 2018).

According to Amoroso – president of Organizzazione di Produttori della Pesca di Trapani – EU regulations in particular have proved too restrictive and have kept changing too quickly to allow small and medium sized companies to adapt their business plans and expectations to the evolving business environment. Moreover, the lack of a clear legislation on wholesale trade has discouraged the expansion of activities to other segments of the production chain. It does not make sense to invest in establishing processing plants or platforms if operators do not converge towards a common wholesale market. Additionally, the proliferation of POs – for example, in the Trapani area there are two POs working in the same fishery segment – has hampered the capacity to facilitate integration across the production chain (Amoroso, 2018). Dilello – President of Cooperativa fra Pescatori “LA SIRENA” – states that other relevant factors limiting structural vertical and horizontal integration include a fragmented and biased domestic regulatory framework, excessively restrictive and insufficiently supporting EU policies, a low degree of market organization and a weak role defined for and played by POs (Dilello, 2018). Misuraca – business consultant of Medipesca – says that historically speaking, contrary to other EU countries such as Spain, Italy has failed to develop a coherent and comprehensive vision of fishery as an economic sector. State authorities have tended to shift competences to regional authorities. This has produced fragmentation in terms of both regulation and market dynamics (Misuraca, 2018).

Dilello argues that the lack of integration is due to the strategic mistake on the part of the EU, which made vessel scrapping its main policy objective and financial target in the form of subsidies for vessel scrapping. He states that the sector has suffered from a serious contraction across the entire value chain. Moreover, POs have not received funding for over two years now, impairing their ability to foster integration (Misuraca, 2018).

Amoroso states that according to a recently conducted study, considering the costs that they have to support, even vessels involved in Bluefin tuna fishing have zero margins of profits. The quota system is too restrictive and too poorly managed to allow any income gains even in a sector potentially as profitable as that of Bluefin tuna (Amoroso, 2018).

0 Comments